My husband works for a startup. Before this one, he worked at another startup. So in our household, we talk about stock options quite a lot. Naturally, our 5-year-old recently started asking what things like “RSUs” are.

Now, explaining equity compensation to adults can already be confusing enough. Explaining it to a 5-year-old is even harder. But since he loves pizza, I thought pizza might be the perfect way to explain the strange world of RSUs, ESPPs, ISOs, NSOs, and other alphabet soup of startup compensation.

So here’s my best attempt to explain equity compensation: pizza style.

Imagine getting a job offer that includes a mysterious locked treasure chest alongside your regular paycheck. Your boss tells you that you cannot open it for a few years, but if the company does well, the contents could eventually be worth more than your car. This is often the reality for employees navigating a startup equity guide for new hires; the cash pays your rent today, but the locked chest represents a chance at future wealth.

Think of the entire company like a giant, delicious pizza that has been cut into millions of tiny slices. In the financial world, we call these slices “shares” or “equity.” When a business offers you equity, they aren't just hiring you to work there; they are actually giving you a small piece of the company itself. While you can't eat this pizza slice, understanding employee equity compensation means realizing that this piece of paper represents ownership that can grow in value over time.

Why would they give away pieces of their pizza instead of just paying you more cash? Business psychology experts have long noted that owners treat things differently than renters do. If you own a slice of the company, you will likely work harder to make sure the whole pizza gets bigger and more valuable, because that makes your specific slice worth more money, too. It transforms you from a regular worker into a partner who benefits when the business wins.

Unfortunately, lawyers and bankers love to use confusing alphabet soup to describe these slices, making it hard to know if you are getting a good deal. To help you find the keys to your treasure chest, we can decode those acronyms so you can stop worrying about the jargon and start understanding how this "funny money" turns into real cash in your bank account.

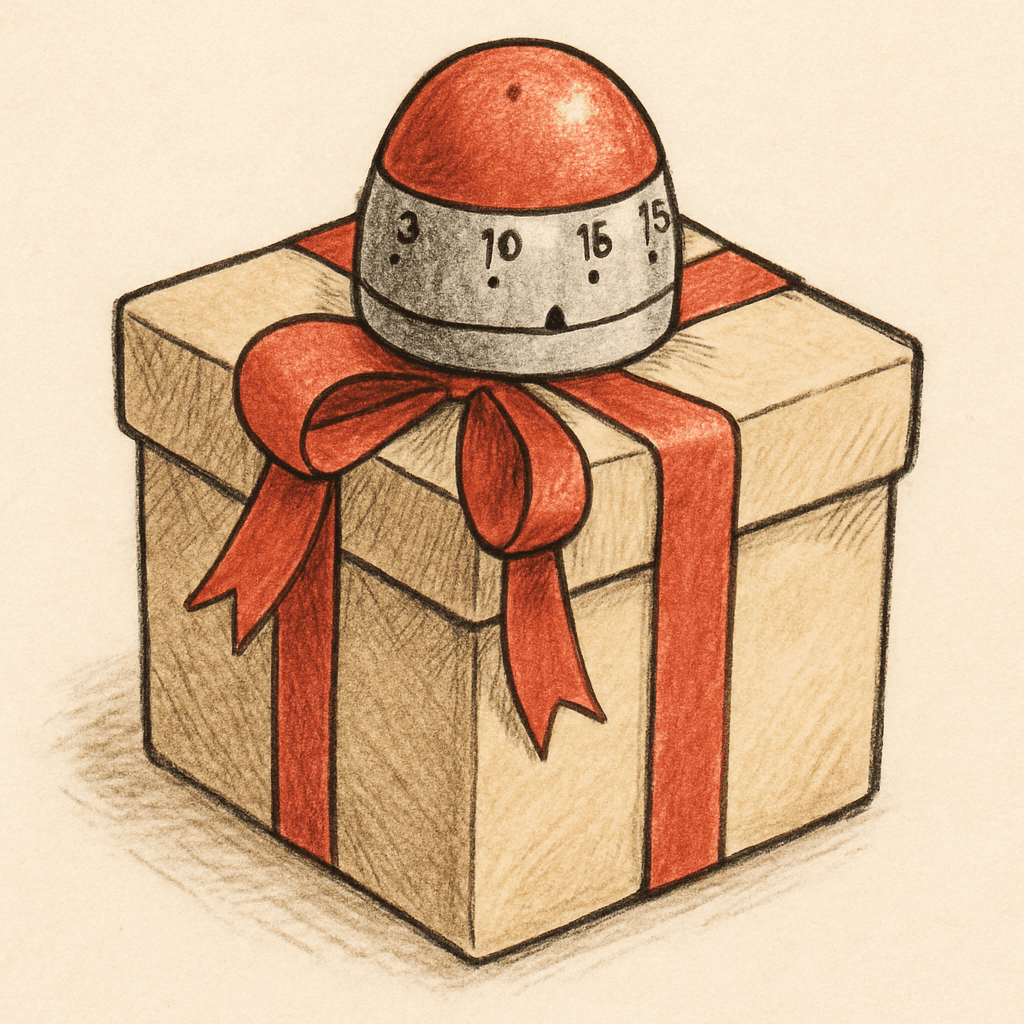

The 'Vesting' Timer: Why You Can’t Eat Your Pizza Slices Right Away

Imagine your boss hands you a whole, freshly baked pizza representing ownership in the company. It looks delicious and has your name on the box, but there is a catch: the box is locked. You can see the pizza, and you know it’s technically yours, but you aren't allowed to eat a single slice yet. This moment, when the company promises you the equity, is called the Grant Date. Companies use this lock to make sure you stick around; they want to reward loyalty over time, rather than handing over a big bonus on your very first day.

The mechanism that unlocks the box is called vesting. Think of this exactly like a kitchen timer sitting on top of that pizza box. As you continue to work at the company, the timer counts down. Slowly, pieces of that equity move from "promised" to "actually yours" in your bank account. Until that timer rings, the shares are just potential value: an incentive to keep you showing up on Monday mornings. If you leave the job before the vesting happens, the company takes the locked box back, and you walk away with nothing.

Most standard agreements include a strict rule for the first year known as The Cliff. This is the biggest hurdle in how vesting schedules work for beginners. If you quit or get fired after 11 months and 29 days, you get zero slices of the pizza. However, the second you cross that one-year anniversary, a huge chunk unlocks all at once—usually 25% of the total grant. It is the company’s way of saying, "Okay, you proved you’re part of the team, so here is your first big reward."

Once you pass that first major milestone, the rest of the shares usually unlock little by little—often every month—like getting a steady stream of dessert. It’s important to understand the difference between cliff vesting vs graded vesting (the gradual monthly part) when managing stock grants for long term wealth. A typical 4-year timeline looks like this:

The Grant Date: You get the promise of 1,000 shares (Day 1).

The Cliff: You get 0 shares for 12 months. On the 1-year anniversary, you suddenly get 250 shares.

Monthly Vesting: Every month after that, you get small batches (about 20 shares) until year 4 is finished.

With the timer understood, let's look at the specific type of "gift" companies usually put inside that box.

RSUs: The Birthday Present on the High Shelf

Restricted Stock Units, or RSUs, are the simplest form of equity because they function exactly like a birthday present sitting on a high shelf. You can see the box, it has your name on it, and you know that once you are tall enough to reach it—meaning you have finished your vesting waiting period—it is yours to keep. The most important thing to understand about an RSU is that you do not have to buy it. The company gives it to you as a part of your compensation package, just like your salary or health insurance. Once the vesting timer dings, those shares are deposited into your brokerage account, and you can sell them for cash in the company's trading window (most public companies have that) or hold onto them if you think they will grow in value or are emotionally attached to the business itself..

When you are calculating the value of restricted stock units, the math is refreshingly simple compared to other financial products. You just multiply the number of shares you have by the current stock price. If you have 10 shares and the stock is trading at $100, you have $1,000 worth of value. This highlights a critical stability when considering RSU vs stock options pros and cons; while other types of equity can become worthless if the company stock price drops, an RSU retains value as long as the company is worth anything at all. Even if that $100 stock drops to $50, your gift is still worth $500. It acts as a safety net, ensuring you almost always walk away with something for your time.

However, the government treats this "gift" exactly like a cash bonus, which brings us to the inevitable reality of taxes. The moment your shares vest and become yours, the IRS views that value as regular income, just as if your boss handed you a paycheck for that amount. Because you haven't actually paid cash for these shares, the entire amount is taxable. To handle this, most companies use a method often called "sell-to-cover." They will automatically keep a portion of your vested shares—usually about 30% to 40%—and sell them instantly to pay the taxes you owe. If you were supposed to get 100 shares, you might only see 65 land in your account, because the other 35 were sent to the IRS on your behalf.

While your offer letter might list a confusing alphabet soup of rsus espps isos nsos ppus, the RSU is usually the foundation because it requires zero financial risk from you. It is the "free" money that rewards you simply for staying employed. But what if you want to be more aggressive and use some of your own paycheck to buy more shares? That brings us to a different mechanism, where the company acts less like a gift-giver and more like a discount store exclusively for employees.

ESPPs: The Secret Sale at the Company Store

Imagine walking into a grocery store where a gallon of milk costs $5 for everyone else, but because you have a special employee badge, you only pay $4.25. That is essentially how an Employee Stock Purchase Plan (ESPP) works. While RSUs are a "gift," an ESPP is an exclusive "sale" just for you. It allows you to take a portion of your own salary to buy company stock at a discount, usually 15% lower than the market price. One of the biggest benefits of employee stock purchase plans is that you are buying an asset with built-in equity; you are practically guaranteed to pay less than the stock is worth the moment you buy it.

Instead of buying the stock instantly like you would on a trading app, the process happens in a specific cycle called an "offering period." Think of this as a subscription season. You don't buy the shares every payday; instead, the company acts like a piggy bank. They take the percentage of cash you pledged from each paycheck and hold it in a safe place until the end of the season.

The typical lifecycle of that subscription season involves:

Enrollment: You tell the company, "Take 5% of my paycheck for the next six months."

Accumulation: The company keeps that cash in a holding account for you (you don't see it in your checking account).

Purchase Date: At the end of the six months, the company takes that pile of cash and buys as many shares as possible at the discounted price.

Where this gets really powerful is a feature called the "lookback provision." Not all plans have it, but the good ones do. The plan looks at the stock price on the first day of the season and the last day of the season, picks the lower price, and then applies your discount to that number. If the stock price doubled during those six months, you still get to buy it based on the old, lower price. This is one of the safest investment strategies available to employees because it protects you if the stock goes down, but amplifies your gain if the stock goes up.

Once the purchase date passes, the shares appear in your account and are yours to control. You can keep them to watch them grow, or sell them immediately to lock in that instant profit. However, you must be mindful of the tax implications of selling ESPP shares. If you sell them right away, the government considers that discount "profit" as regular income, just like your salary. If you hold onto them for a year or more, you might pay lower taxes. But while ESPPs involve buying stock directly, there is another form of equity that acts more like a "reservation" for stock in the future.

Stock Options: The Magic Coupons for Future Pizza

Imagine you love a local pizza place where a slice currently costs $2. The owner likes you, so she hands you a special golden ticket. This ticket says, "No matter what happens in the future, you have the right to buy a slice of pizza from me for just $1." Five years pass. The pizza place becomes world-famous, and a single slice now costs $10. Your ticket is still valid. You hand over your $1, get the $10 slice, and instantly hold $9 of pure value.

That is exactly how a stock option works. It is not the stock itself; it is a contract that "freezes" the price for you. In the financial world, that frozen price on your ticket is called the "Strike Price" (or Grant Price). When you join a company, they set this price based on what the company is currently worth. For startups, this number is determined by the fair market value of private company stock, which is often very low—sometimes just pennies per share. The goal is simple: you want the company's value to go up while your strike price stays exactly the same. The difference between your low strike price and the high market price is your profit, often called "the spread."

Unlike the "gift" of RSUs or the "discount" of ESPPs, options require you to spend your own money to get the asset. Using your coupon to officially buy the shares is called "exercising" your options. You pay the strike price multiplied by the number of shares you want. This creates a strategic choice: when should you buy? Many employees wait until the company goes public so they can sell the shares immediately to cover the cost. However, if you are planning for the long term, learning how to exercise incentive stock options early can sometimes offer tax benefits, though it carries the risk that you might buy stock that later decreases in value.

Why would anyone want a coupon that costs money instead of a free gift like an RSU? It usually comes down to "leverage"—the potential for a massive payout. Because options require you to put skin in the game, companies generally grant far more options than they would RSUs. When looking at RSU vs stock options pros and cons, it helps to view them side-by-side:

RSUs (The Gift): You pay $0. You receive fewer shares. Low risk (even if the stock price drops, the shares are still worth something).

Options (The Coupon): You pay the Strike Price. You receive more shares. High risk (if the stock price drops below your strike price, your coupon is worthless), but potentially much higher reward.

Owning options feels a bit like holding a lottery ticket where you have some control over the outcome. You have the right to buy in at the ground floor, even if the building is now a skyscraper. However, not all coupons are printed the same way. The government actually has two different classifications for these options—ISOs and NSOs—and the one you have in your offer letter will dictate whether the IRS takes a small bite or a large chunk of your future pizza.

ISOs vs. NSOs: Why the Government Treats Your Coupons Differently

Check your specific grant paperwork to see which acronym sits next to your number of shares, as this tiny label determines how much of your profit you actually get to keep. Incentive Stock Options (ISOs) are essentially the "VIP coupons" generally reserved exclusively for full-time employees. The government offers these with a significant tax advantage to encourage long-term loyalty to the company. On the flip side, Non-Qualified Stock Options (NSOs) are the standard version given to outside consultants, board members, and often employees as well. When you finally use an NSO coupon to buy your shares, the government views your "discount" exactly like a cash bonus, meaning it is taxed immediately at your regular income tax rate.

Patience is the secret ingredient that makes the VIP version so powerful. To unlock the tax benefits of an ISO, you generally must buy the stock and then hold onto it for at least a year before selling. If you follow these rules, your profit is taxed at the much lower "capital gains" rate, which can save you a massive amount of money compared to regular income tax. However, there is a hidden catch known as the impact of alternative minimum tax on ISOs. This complex rule ensures that high earners pay at least a minimum amount of tax, and it can sometimes surprise employees who buy a large number of ISOs without selling them immediately. It is always wise to ask a tax professional to run the numbers before you buy to ensure you don't get a surprise bill from the IRS in April.

Knowing the difference between ISO and NSO tax treatment helps you plan your financial future, but don't worry if your offer letter lists NSOs. A simple explanation of qualified vs non-qualified stock options reveals that while NSOs require you to pay taxes sooner, they are also much simpler to manage and don't carry the same complex holding risks as ISOs. Both types give you the right to own a piece of the company pie. Yet, some unique private companies skip the concept of owning shares entirely, instead offering a system that looks more like a scoreboard than a stock portfolio.

PPUs: The 'Scoreboard' Slices for Private Teams

Imagine playing an arcade game where you collect paper tickets instead of keeping the actual prizes on the shelf. You don't own the giant teddy bear behind the counter yet, but those tickets hold the promise that you can trade them in for value later. This is exactly how Profit Participation Units (PPUs) work. For those wondering what are PPUs for employees, think of them as a cash bonus that tracks the company’s success. You don't get a real share of stock—you get a "shadow" share that mimics the price. If the company value goes up, your bonus goes up, but you never have to worry about buying or holding actual certificates.

PPUs aren't commonly seen as the others mentioned above and mostly known for being heavily used by OpenAI. Since the company isn't listed on a public stock market yet, there is no store where you can sell your shares today. Instead, you are waiting for a specific moment called a "liquidity event." Think of this like the company selling the entire arcade to a new owner. When that big sale happens, the new owners look at your scoreboard, calculate what your PPUs are worth based on the final sale price, and pay you out in cash. This distinction is essential in any startup equity guide for new hires, as it means your payout is strictly tied to the company being sold or going public.

The best part about this "shadow" equity is that it usually requires zero work from you. Unlike the complex coupons we discussed earlier where you have to spend your own money to buy shares, PPUs simply convert into a check when the time comes. While the alphabet soup of rsus, espps, isos, and nsos, remember that PPUs are just a promised future bonus. Once you understand which type of reward you are holding, the only question left is understanding the mechanics of that final payday.

When to Trade Your Paper for Gold: Turning Equity into Cash

Having all your money in your employer's stock is like packing a lunchbox entirely with chocolate bars. It looks amazing at first, but if you suddenly need a sandwich or a bottle of water, you are out of luck. If your company hits a rough patch, you risk losing both your weekly paycheck and your savings at the same time. This is why financial experts talk about investment strategies like "diversification." It is just a fancy word for not keeping all your eggs in one basket. By selling some of your company shares, you can use that cash to buy different things—like a house or shares in other companies—ensuring your financial health survives even if your employer has a bad year.

Once you decide to swap your shares for cash, you must pass through a mandatory toll booth. The government treats the profit you make from selling stock essentially the same way it treats your salary: as income that must be taxed. These tax implications mean you won't keep every single penny of the sale price. Your company might automatically withhold a portion of the money to pay the IRS, or you might owe it later when you file your annual tax return. While seeing a smaller number hit your bank account can be annoying, remember that paying taxes is actually a good sign—it means you made a profit.

Deciding exactly when to sell can feel like guessing, but you don't need a crystal ball to get it right. Managing stock grants for long term wealth is less about predicting the stock market and more about looking at your own life. You should consider trading your paper equity for real cash when:

You Have a Goal: You need the money for a tangible "life upgrade," such as a down payment on a house, a new car, or paying off student loans.

You Are Overloaded: Your company stock takes up more than 5% or 10% of your total savings, making your "lunchbox" too risky.

You Want Stability: You prefer to move the money into a general retirement fund that grows slowly and safely over time.

Read more

My husband works for a startup. Before this one, he worked at another startup. So in our household, we talk about stock options quite a lot. Naturally, our 5-year-old recently started asking what things like “RSUs” are.

Now, explaining equity compensation to adults can already be confusing enough. Explaining it to a 5-year-old is even harder. But since he loves pizza, I thought pizza might be the perfect way to explain the strange world of RSUs, ESPPs, ISOs, NSOs, and other alphabet soup of startup compensation.

So here’s my best attempt to explain equity compensation: pizza style.

Imagine getting a job offer that includes a mysterious locked treasure chest alongside your regular paycheck. Your boss tells you that you cannot open it for a few years, but if the company does well, the contents could eventually be worth more than your car. This is often the reality for employees navigating a startup equity guide for new hires; the cash pays your rent today, but the locked chest represents a chance at future wealth.

Think of the entire company like a giant, delicious pizza that has been cut into millions of tiny slices. In the financial world, we call these slices “shares” or “equity.” When a business offers you equity, they aren't just hiring you to work there; they are actually giving you a small piece of the company itself. While you can't eat this pizza slice, understanding employee equity compensation means realizing that this piece of paper represents ownership that can grow in value over time.

Why would they give away pieces of their pizza instead of just paying you more cash? Business psychology experts have long noted that owners treat things differently than renters do. If you own a slice of the company, you will likely work harder to make sure the whole pizza gets bigger and more valuable, because that makes your specific slice worth more money, too. It transforms you from a regular worker into a partner who benefits when the business wins.

Unfortunately, lawyers and bankers love to use confusing alphabet soup to describe these slices, making it hard to know if you are getting a good deal. To help you find the keys to your treasure chest, we can decode those acronyms so you can stop worrying about the jargon and start understanding how this "funny money" turns into real cash in your bank account.

The 'Vesting' Timer: Why You Can’t Eat Your Pizza Slices Right Away

Imagine your boss hands you a whole, freshly baked pizza representing ownership in the company. It looks delicious and has your name on the box, but there is a catch: the box is locked. You can see the pizza, and you know it’s technically yours, but you aren't allowed to eat a single slice yet. This moment, when the company promises you the equity, is called the Grant Date. Companies use this lock to make sure you stick around; they want to reward loyalty over time, rather than handing over a big bonus on your very first day.

The mechanism that unlocks the box is called vesting. Think of this exactly like a kitchen timer sitting on top of that pizza box. As you continue to work at the company, the timer counts down. Slowly, pieces of that equity move from "promised" to "actually yours" in your bank account. Until that timer rings, the shares are just potential value: an incentive to keep you showing up on Monday mornings. If you leave the job before the vesting happens, the company takes the locked box back, and you walk away with nothing.

Most standard agreements include a strict rule for the first year known as The Cliff. This is the biggest hurdle in how vesting schedules work for beginners. If you quit or get fired after 11 months and 29 days, you get zero slices of the pizza. However, the second you cross that one-year anniversary, a huge chunk unlocks all at once—usually 25% of the total grant. It is the company’s way of saying, "Okay, you proved you’re part of the team, so here is your first big reward."

Once you pass that first major milestone, the rest of the shares usually unlock little by little—often every month—like getting a steady stream of dessert. It’s important to understand the difference between cliff vesting vs graded vesting (the gradual monthly part) when managing stock grants for long term wealth. A typical 4-year timeline looks like this:

The Grant Date: You get the promise of 1,000 shares (Day 1).

The Cliff: You get 0 shares for 12 months. On the 1-year anniversary, you suddenly get 250 shares.

Monthly Vesting: Every month after that, you get small batches (about 20 shares) until year 4 is finished.

With the timer understood, let's look at the specific type of "gift" companies usually put inside that box.

RSUs: The Birthday Present on the High Shelf

Restricted Stock Units, or RSUs, are the simplest form of equity because they function exactly like a birthday present sitting on a high shelf. You can see the box, it has your name on it, and you know that once you are tall enough to reach it—meaning you have finished your vesting waiting period—it is yours to keep. The most important thing to understand about an RSU is that you do not have to buy it. The company gives it to you as a part of your compensation package, just like your salary or health insurance. Once the vesting timer dings, those shares are deposited into your brokerage account, and you can sell them for cash in the company's trading window (most public companies have that) or hold onto them if you think they will grow in value or are emotionally attached to the business itself..

When you are calculating the value of restricted stock units, the math is refreshingly simple compared to other financial products. You just multiply the number of shares you have by the current stock price. If you have 10 shares and the stock is trading at $100, you have $1,000 worth of value. This highlights a critical stability when considering RSU vs stock options pros and cons; while other types of equity can become worthless if the company stock price drops, an RSU retains value as long as the company is worth anything at all. Even if that $100 stock drops to $50, your gift is still worth $500. It acts as a safety net, ensuring you almost always walk away with something for your time.

However, the government treats this "gift" exactly like a cash bonus, which brings us to the inevitable reality of taxes. The moment your shares vest and become yours, the IRS views that value as regular income, just as if your boss handed you a paycheck for that amount. Because you haven't actually paid cash for these shares, the entire amount is taxable. To handle this, most companies use a method often called "sell-to-cover." They will automatically keep a portion of your vested shares—usually about 30% to 40%—and sell them instantly to pay the taxes you owe. If you were supposed to get 100 shares, you might only see 65 land in your account, because the other 35 were sent to the IRS on your behalf.

While your offer letter might list a confusing alphabet soup of rsus espps isos nsos ppus, the RSU is usually the foundation because it requires zero financial risk from you. It is the "free" money that rewards you simply for staying employed. But what if you want to be more aggressive and use some of your own paycheck to buy more shares? That brings us to a different mechanism, where the company acts less like a gift-giver and more like a discount store exclusively for employees.

ESPPs: The Secret Sale at the Company Store

Imagine walking into a grocery store where a gallon of milk costs $5 for everyone else, but because you have a special employee badge, you only pay $4.25. That is essentially how an Employee Stock Purchase Plan (ESPP) works. While RSUs are a "gift," an ESPP is an exclusive "sale" just for you. It allows you to take a portion of your own salary to buy company stock at a discount, usually 15% lower than the market price. One of the biggest benefits of employee stock purchase plans is that you are buying an asset with built-in equity; you are practically guaranteed to pay less than the stock is worth the moment you buy it.

Instead of buying the stock instantly like you would on a trading app, the process happens in a specific cycle called an "offering period." Think of this as a subscription season. You don't buy the shares every payday; instead, the company acts like a piggy bank. They take the percentage of cash you pledged from each paycheck and hold it in a safe place until the end of the season.

The typical lifecycle of that subscription season involves:

Enrollment: You tell the company, "Take 5% of my paycheck for the next six months."

Accumulation: The company keeps that cash in a holding account for you (you don't see it in your checking account).

Purchase Date: At the end of the six months, the company takes that pile of cash and buys as many shares as possible at the discounted price.

Where this gets really powerful is a feature called the "lookback provision." Not all plans have it, but the good ones do. The plan looks at the stock price on the first day of the season and the last day of the season, picks the lower price, and then applies your discount to that number. If the stock price doubled during those six months, you still get to buy it based on the old, lower price. This is one of the safest investment strategies available to employees because it protects you if the stock goes down, but amplifies your gain if the stock goes up.

Once the purchase date passes, the shares appear in your account and are yours to control. You can keep them to watch them grow, or sell them immediately to lock in that instant profit. However, you must be mindful of the tax implications of selling ESPP shares. If you sell them right away, the government considers that discount "profit" as regular income, just like your salary. If you hold onto them for a year or more, you might pay lower taxes. But while ESPPs involve buying stock directly, there is another form of equity that acts more like a "reservation" for stock in the future.

Stock Options: The Magic Coupons for Future Pizza

Imagine you love a local pizza place where a slice currently costs $2. The owner likes you, so she hands you a special golden ticket. This ticket says, "No matter what happens in the future, you have the right to buy a slice of pizza from me for just $1." Five years pass. The pizza place becomes world-famous, and a single slice now costs $10. Your ticket is still valid. You hand over your $1, get the $10 slice, and instantly hold $9 of pure value.

That is exactly how a stock option works. It is not the stock itself; it is a contract that "freezes" the price for you. In the financial world, that frozen price on your ticket is called the "Strike Price" (or Grant Price). When you join a company, they set this price based on what the company is currently worth. For startups, this number is determined by the fair market value of private company stock, which is often very low—sometimes just pennies per share. The goal is simple: you want the company's value to go up while your strike price stays exactly the same. The difference between your low strike price and the high market price is your profit, often called "the spread."

Unlike the "gift" of RSUs or the "discount" of ESPPs, options require you to spend your own money to get the asset. Using your coupon to officially buy the shares is called "exercising" your options. You pay the strike price multiplied by the number of shares you want. This creates a strategic choice: when should you buy? Many employees wait until the company goes public so they can sell the shares immediately to cover the cost. However, if you are planning for the long term, learning how to exercise incentive stock options early can sometimes offer tax benefits, though it carries the risk that you might buy stock that later decreases in value.

Why would anyone want a coupon that costs money instead of a free gift like an RSU? It usually comes down to "leverage"—the potential for a massive payout. Because options require you to put skin in the game, companies generally grant far more options than they would RSUs. When looking at RSU vs stock options pros and cons, it helps to view them side-by-side:

RSUs (The Gift): You pay $0. You receive fewer shares. Low risk (even if the stock price drops, the shares are still worth something).

Options (The Coupon): You pay the Strike Price. You receive more shares. High risk (if the stock price drops below your strike price, your coupon is worthless), but potentially much higher reward.

Owning options feels a bit like holding a lottery ticket where you have some control over the outcome. You have the right to buy in at the ground floor, even if the building is now a skyscraper. However, not all coupons are printed the same way. The government actually has two different classifications for these options—ISOs and NSOs—and the one you have in your offer letter will dictate whether the IRS takes a small bite or a large chunk of your future pizza.

ISOs vs. NSOs: Why the Government Treats Your Coupons Differently

Check your specific grant paperwork to see which acronym sits next to your number of shares, as this tiny label determines how much of your profit you actually get to keep. Incentive Stock Options (ISOs) are essentially the "VIP coupons" generally reserved exclusively for full-time employees. The government offers these with a significant tax advantage to encourage long-term loyalty to the company. On the flip side, Non-Qualified Stock Options (NSOs) are the standard version given to outside consultants, board members, and often employees as well. When you finally use an NSO coupon to buy your shares, the government views your "discount" exactly like a cash bonus, meaning it is taxed immediately at your regular income tax rate.

Patience is the secret ingredient that makes the VIP version so powerful. To unlock the tax benefits of an ISO, you generally must buy the stock and then hold onto it for at least a year before selling. If you follow these rules, your profit is taxed at the much lower "capital gains" rate, which can save you a massive amount of money compared to regular income tax. However, there is a hidden catch known as the impact of alternative minimum tax on ISOs. This complex rule ensures that high earners pay at least a minimum amount of tax, and it can sometimes surprise employees who buy a large number of ISOs without selling them immediately. It is always wise to ask a tax professional to run the numbers before you buy to ensure you don't get a surprise bill from the IRS in April.

Knowing the difference between ISO and NSO tax treatment helps you plan your financial future, but don't worry if your offer letter lists NSOs. A simple explanation of qualified vs non-qualified stock options reveals that while NSOs require you to pay taxes sooner, they are also much simpler to manage and don't carry the same complex holding risks as ISOs. Both types give you the right to own a piece of the company pie. Yet, some unique private companies skip the concept of owning shares entirely, instead offering a system that looks more like a scoreboard than a stock portfolio.

PPUs: The 'Scoreboard' Slices for Private Teams

Imagine playing an arcade game where you collect paper tickets instead of keeping the actual prizes on the shelf. You don't own the giant teddy bear behind the counter yet, but those tickets hold the promise that you can trade them in for value later. This is exactly how Profit Participation Units (PPUs) work. For those wondering what are PPUs for employees, think of them as a cash bonus that tracks the company’s success. You don't get a real share of stock—you get a "shadow" share that mimics the price. If the company value goes up, your bonus goes up, but you never have to worry about buying or holding actual certificates.

PPUs aren't commonly seen as the others mentioned above and mostly known for being heavily used by OpenAI. Since the company isn't listed on a public stock market yet, there is no store where you can sell your shares today. Instead, you are waiting for a specific moment called a "liquidity event." Think of this like the company selling the entire arcade to a new owner. When that big sale happens, the new owners look at your scoreboard, calculate what your PPUs are worth based on the final sale price, and pay you out in cash. This distinction is essential in any startup equity guide for new hires, as it means your payout is strictly tied to the company being sold or going public.

The best part about this "shadow" equity is that it usually requires zero work from you. Unlike the complex coupons we discussed earlier where you have to spend your own money to buy shares, PPUs simply convert into a check when the time comes. While the alphabet soup of rsus, espps, isos, and nsos, remember that PPUs are just a promised future bonus. Once you understand which type of reward you are holding, the only question left is understanding the mechanics of that final payday.

When to Trade Your Paper for Gold: Turning Equity into Cash

Having all your money in your employer's stock is like packing a lunchbox entirely with chocolate bars. It looks amazing at first, but if you suddenly need a sandwich or a bottle of water, you are out of luck. If your company hits a rough patch, you risk losing both your weekly paycheck and your savings at the same time. This is why financial experts talk about investment strategies like "diversification." It is just a fancy word for not keeping all your eggs in one basket. By selling some of your company shares, you can use that cash to buy different things—like a house or shares in other companies—ensuring your financial health survives even if your employer has a bad year.

Once you decide to swap your shares for cash, you must pass through a mandatory toll booth. The government treats the profit you make from selling stock essentially the same way it treats your salary: as income that must be taxed. These tax implications mean you won't keep every single penny of the sale price. Your company might automatically withhold a portion of the money to pay the IRS, or you might owe it later when you file your annual tax return. While seeing a smaller number hit your bank account can be annoying, remember that paying taxes is actually a good sign—it means you made a profit.

Deciding exactly when to sell can feel like guessing, but you don't need a crystal ball to get it right. Managing stock grants for long term wealth is less about predicting the stock market and more about looking at your own life. You should consider trading your paper equity for real cash when:

You Have a Goal: You need the money for a tangible "life upgrade," such as a down payment on a house, a new car, or paying off student loans.

You Are Overloaded: Your company stock takes up more than 5% or 10% of your total savings, making your "lunchbox" too risky.

You Want Stability: You prefer to move the money into a general retirement fund that grows slowly and safely over time.

Read more

My husband works for a startup. Before this one, he worked at another startup. So in our household, we talk about stock options quite a lot. Naturally, our 5-year-old recently started asking what things like “RSUs” are.

Now, explaining equity compensation to adults can already be confusing enough. Explaining it to a 5-year-old is even harder. But since he loves pizza, I thought pizza might be the perfect way to explain the strange world of RSUs, ESPPs, ISOs, NSOs, and other alphabet soup of startup compensation.

So here’s my best attempt to explain equity compensation: pizza style.

Imagine getting a job offer that includes a mysterious locked treasure chest alongside your regular paycheck. Your boss tells you that you cannot open it for a few years, but if the company does well, the contents could eventually be worth more than your car. This is often the reality for employees navigating a startup equity guide for new hires; the cash pays your rent today, but the locked chest represents a chance at future wealth.

Think of the entire company like a giant, delicious pizza that has been cut into millions of tiny slices. In the financial world, we call these slices “shares” or “equity.” When a business offers you equity, they aren't just hiring you to work there; they are actually giving you a small piece of the company itself. While you can't eat this pizza slice, understanding employee equity compensation means realizing that this piece of paper represents ownership that can grow in value over time.

Why would they give away pieces of their pizza instead of just paying you more cash? Business psychology experts have long noted that owners treat things differently than renters do. If you own a slice of the company, you will likely work harder to make sure the whole pizza gets bigger and more valuable, because that makes your specific slice worth more money, too. It transforms you from a regular worker into a partner who benefits when the business wins.

Unfortunately, lawyers and bankers love to use confusing alphabet soup to describe these slices, making it hard to know if you are getting a good deal. To help you find the keys to your treasure chest, we can decode those acronyms so you can stop worrying about the jargon and start understanding how this "funny money" turns into real cash in your bank account.

The 'Vesting' Timer: Why You Can’t Eat Your Pizza Slices Right Away

Imagine your boss hands you a whole, freshly baked pizza representing ownership in the company. It looks delicious and has your name on the box, but there is a catch: the box is locked. You can see the pizza, and you know it’s technically yours, but you aren't allowed to eat a single slice yet. This moment, when the company promises you the equity, is called the Grant Date. Companies use this lock to make sure you stick around; they want to reward loyalty over time, rather than handing over a big bonus on your very first day.

The mechanism that unlocks the box is called vesting. Think of this exactly like a kitchen timer sitting on top of that pizza box. As you continue to work at the company, the timer counts down. Slowly, pieces of that equity move from "promised" to "actually yours" in your bank account. Until that timer rings, the shares are just potential value: an incentive to keep you showing up on Monday mornings. If you leave the job before the vesting happens, the company takes the locked box back, and you walk away with nothing.

Most standard agreements include a strict rule for the first year known as The Cliff. This is the biggest hurdle in how vesting schedules work for beginners. If you quit or get fired after 11 months and 29 days, you get zero slices of the pizza. However, the second you cross that one-year anniversary, a huge chunk unlocks all at once—usually 25% of the total grant. It is the company’s way of saying, "Okay, you proved you’re part of the team, so here is your first big reward."

Once you pass that first major milestone, the rest of the shares usually unlock little by little—often every month—like getting a steady stream of dessert. It’s important to understand the difference between cliff vesting vs graded vesting (the gradual monthly part) when managing stock grants for long term wealth. A typical 4-year timeline looks like this:

The Grant Date: You get the promise of 1,000 shares (Day 1).

The Cliff: You get 0 shares for 12 months. On the 1-year anniversary, you suddenly get 250 shares.

Monthly Vesting: Every month after that, you get small batches (about 20 shares) until year 4 is finished.

With the timer understood, let's look at the specific type of "gift" companies usually put inside that box.

RSUs: The Birthday Present on the High Shelf

Restricted Stock Units, or RSUs, are the simplest form of equity because they function exactly like a birthday present sitting on a high shelf. You can see the box, it has your name on it, and you know that once you are tall enough to reach it—meaning you have finished your vesting waiting period—it is yours to keep. The most important thing to understand about an RSU is that you do not have to buy it. The company gives it to you as a part of your compensation package, just like your salary or health insurance. Once the vesting timer dings, those shares are deposited into your brokerage account, and you can sell them for cash in the company's trading window (most public companies have that) or hold onto them if you think they will grow in value or are emotionally attached to the business itself..

When you are calculating the value of restricted stock units, the math is refreshingly simple compared to other financial products. You just multiply the number of shares you have by the current stock price. If you have 10 shares and the stock is trading at $100, you have $1,000 worth of value. This highlights a critical stability when considering RSU vs stock options pros and cons; while other types of equity can become worthless if the company stock price drops, an RSU retains value as long as the company is worth anything at all. Even if that $100 stock drops to $50, your gift is still worth $500. It acts as a safety net, ensuring you almost always walk away with something for your time.

However, the government treats this "gift" exactly like a cash bonus, which brings us to the inevitable reality of taxes. The moment your shares vest and become yours, the IRS views that value as regular income, just as if your boss handed you a paycheck for that amount. Because you haven't actually paid cash for these shares, the entire amount is taxable. To handle this, most companies use a method often called "sell-to-cover." They will automatically keep a portion of your vested shares—usually about 30% to 40%—and sell them instantly to pay the taxes you owe. If you were supposed to get 100 shares, you might only see 65 land in your account, because the other 35 were sent to the IRS on your behalf.

While your offer letter might list a confusing alphabet soup of rsus espps isos nsos ppus, the RSU is usually the foundation because it requires zero financial risk from you. It is the "free" money that rewards you simply for staying employed. But what if you want to be more aggressive and use some of your own paycheck to buy more shares? That brings us to a different mechanism, where the company acts less like a gift-giver and more like a discount store exclusively for employees.

ESPPs: The Secret Sale at the Company Store

Imagine walking into a grocery store where a gallon of milk costs $5 for everyone else, but because you have a special employee badge, you only pay $4.25. That is essentially how an Employee Stock Purchase Plan (ESPP) works. While RSUs are a "gift," an ESPP is an exclusive "sale" just for you. It allows you to take a portion of your own salary to buy company stock at a discount, usually 15% lower than the market price. One of the biggest benefits of employee stock purchase plans is that you are buying an asset with built-in equity; you are practically guaranteed to pay less than the stock is worth the moment you buy it.

Instead of buying the stock instantly like you would on a trading app, the process happens in a specific cycle called an "offering period." Think of this as a subscription season. You don't buy the shares every payday; instead, the company acts like a piggy bank. They take the percentage of cash you pledged from each paycheck and hold it in a safe place until the end of the season.

The typical lifecycle of that subscription season involves:

Enrollment: You tell the company, "Take 5% of my paycheck for the next six months."

Accumulation: The company keeps that cash in a holding account for you (you don't see it in your checking account).

Purchase Date: At the end of the six months, the company takes that pile of cash and buys as many shares as possible at the discounted price.

Where this gets really powerful is a feature called the "lookback provision." Not all plans have it, but the good ones do. The plan looks at the stock price on the first day of the season and the last day of the season, picks the lower price, and then applies your discount to that number. If the stock price doubled during those six months, you still get to buy it based on the old, lower price. This is one of the safest investment strategies available to employees because it protects you if the stock goes down, but amplifies your gain if the stock goes up.

Once the purchase date passes, the shares appear in your account and are yours to control. You can keep them to watch them grow, or sell them immediately to lock in that instant profit. However, you must be mindful of the tax implications of selling ESPP shares. If you sell them right away, the government considers that discount "profit" as regular income, just like your salary. If you hold onto them for a year or more, you might pay lower taxes. But while ESPPs involve buying stock directly, there is another form of equity that acts more like a "reservation" for stock in the future.

Stock Options: The Magic Coupons for Future Pizza

Imagine you love a local pizza place where a slice currently costs $2. The owner likes you, so she hands you a special golden ticket. This ticket says, "No matter what happens in the future, you have the right to buy a slice of pizza from me for just $1." Five years pass. The pizza place becomes world-famous, and a single slice now costs $10. Your ticket is still valid. You hand over your $1, get the $10 slice, and instantly hold $9 of pure value.

That is exactly how a stock option works. It is not the stock itself; it is a contract that "freezes" the price for you. In the financial world, that frozen price on your ticket is called the "Strike Price" (or Grant Price). When you join a company, they set this price based on what the company is currently worth. For startups, this number is determined by the fair market value of private company stock, which is often very low—sometimes just pennies per share. The goal is simple: you want the company's value to go up while your strike price stays exactly the same. The difference between your low strike price and the high market price is your profit, often called "the spread."

Unlike the "gift" of RSUs or the "discount" of ESPPs, options require you to spend your own money to get the asset. Using your coupon to officially buy the shares is called "exercising" your options. You pay the strike price multiplied by the number of shares you want. This creates a strategic choice: when should you buy? Many employees wait until the company goes public so they can sell the shares immediately to cover the cost. However, if you are planning for the long term, learning how to exercise incentive stock options early can sometimes offer tax benefits, though it carries the risk that you might buy stock that later decreases in value.

Why would anyone want a coupon that costs money instead of a free gift like an RSU? It usually comes down to "leverage"—the potential for a massive payout. Because options require you to put skin in the game, companies generally grant far more options than they would RSUs. When looking at RSU vs stock options pros and cons, it helps to view them side-by-side:

RSUs (The Gift): You pay $0. You receive fewer shares. Low risk (even if the stock price drops, the shares are still worth something).

Options (The Coupon): You pay the Strike Price. You receive more shares. High risk (if the stock price drops below your strike price, your coupon is worthless), but potentially much higher reward.

Owning options feels a bit like holding a lottery ticket where you have some control over the outcome. You have the right to buy in at the ground floor, even if the building is now a skyscraper. However, not all coupons are printed the same way. The government actually has two different classifications for these options—ISOs and NSOs—and the one you have in your offer letter will dictate whether the IRS takes a small bite or a large chunk of your future pizza.

ISOs vs. NSOs: Why the Government Treats Your Coupons Differently

Check your specific grant paperwork to see which acronym sits next to your number of shares, as this tiny label determines how much of your profit you actually get to keep. Incentive Stock Options (ISOs) are essentially the "VIP coupons" generally reserved exclusively for full-time employees. The government offers these with a significant tax advantage to encourage long-term loyalty to the company. On the flip side, Non-Qualified Stock Options (NSOs) are the standard version given to outside consultants, board members, and often employees as well. When you finally use an NSO coupon to buy your shares, the government views your "discount" exactly like a cash bonus, meaning it is taxed immediately at your regular income tax rate.

Patience is the secret ingredient that makes the VIP version so powerful. To unlock the tax benefits of an ISO, you generally must buy the stock and then hold onto it for at least a year before selling. If you follow these rules, your profit is taxed at the much lower "capital gains" rate, which can save you a massive amount of money compared to regular income tax. However, there is a hidden catch known as the impact of alternative minimum tax on ISOs. This complex rule ensures that high earners pay at least a minimum amount of tax, and it can sometimes surprise employees who buy a large number of ISOs without selling them immediately. It is always wise to ask a tax professional to run the numbers before you buy to ensure you don't get a surprise bill from the IRS in April.

Knowing the difference between ISO and NSO tax treatment helps you plan your financial future, but don't worry if your offer letter lists NSOs. A simple explanation of qualified vs non-qualified stock options reveals that while NSOs require you to pay taxes sooner, they are also much simpler to manage and don't carry the same complex holding risks as ISOs. Both types give you the right to own a piece of the company pie. Yet, some unique private companies skip the concept of owning shares entirely, instead offering a system that looks more like a scoreboard than a stock portfolio.

PPUs: The 'Scoreboard' Slices for Private Teams

Imagine playing an arcade game where you collect paper tickets instead of keeping the actual prizes on the shelf. You don't own the giant teddy bear behind the counter yet, but those tickets hold the promise that you can trade them in for value later. This is exactly how Profit Participation Units (PPUs) work. For those wondering what are PPUs for employees, think of them as a cash bonus that tracks the company’s success. You don't get a real share of stock—you get a "shadow" share that mimics the price. If the company value goes up, your bonus goes up, but you never have to worry about buying or holding actual certificates.

PPUs aren't commonly seen as the others mentioned above and mostly known for being heavily used by OpenAI. Since the company isn't listed on a public stock market yet, there is no store where you can sell your shares today. Instead, you are waiting for a specific moment called a "liquidity event." Think of this like the company selling the entire arcade to a new owner. When that big sale happens, the new owners look at your scoreboard, calculate what your PPUs are worth based on the final sale price, and pay you out in cash. This distinction is essential in any startup equity guide for new hires, as it means your payout is strictly tied to the company being sold or going public.

The best part about this "shadow" equity is that it usually requires zero work from you. Unlike the complex coupons we discussed earlier where you have to spend your own money to buy shares, PPUs simply convert into a check when the time comes. While the alphabet soup of rsus, espps, isos, and nsos, remember that PPUs are just a promised future bonus. Once you understand which type of reward you are holding, the only question left is understanding the mechanics of that final payday.

When to Trade Your Paper for Gold: Turning Equity into Cash

Having all your money in your employer's stock is like packing a lunchbox entirely with chocolate bars. It looks amazing at first, but if you suddenly need a sandwich or a bottle of water, you are out of luck. If your company hits a rough patch, you risk losing both your weekly paycheck and your savings at the same time. This is why financial experts talk about investment strategies like "diversification." It is just a fancy word for not keeping all your eggs in one basket. By selling some of your company shares, you can use that cash to buy different things—like a house or shares in other companies—ensuring your financial health survives even if your employer has a bad year.

Once you decide to swap your shares for cash, you must pass through a mandatory toll booth. The government treats the profit you make from selling stock essentially the same way it treats your salary: as income that must be taxed. These tax implications mean you won't keep every single penny of the sale price. Your company might automatically withhold a portion of the money to pay the IRS, or you might owe it later when you file your annual tax return. While seeing a smaller number hit your bank account can be annoying, remember that paying taxes is actually a good sign—it means you made a profit.

Deciding exactly when to sell can feel like guessing, but you don't need a crystal ball to get it right. Managing stock grants for long term wealth is less about predicting the stock market and more about looking at your own life. You should consider trading your paper equity for real cash when:

You Have a Goal: You need the money for a tangible "life upgrade," such as a down payment on a house, a new car, or paying off student loans.

You Are Overloaded: Your company stock takes up more than 5% or 10% of your total savings, making your "lunchbox" too risky.

You Want Stability: You prefer to move the money into a general retirement fund that grows slowly and safely over time.